In 1994, Congress passed a landmark law that allowed America’s banks to merge across state lines with few restrictions. To allay fears that the industry’s whales would become far bigger and even more powerful, the measure limited the total share of the nation’s deposits that any one entity could hold to 10%, as well as restricting the percentage within a state to 30%. The cap applied only to acquisitions; the giant lenders that advanced over the threshold could compete for new deposits via organic growth without facing any limits on their share of the total. By 2014, the nation’s three largest players, JPMorgan Chase, Bank of America and Wells Fargo, had grown quickly—in part via their respective rescues of Washington Mutual, Merrill Lynch and Wachovia in the Great Financial Crisis—to exceed the 10% ceiling. Hence, the rule has essentially blocked the three behemoths from acquiring any rival lenders for a decade.

The 1994 act, however, provided a loophole that allowed waivers from the 10% maximum for buyers that stepped up to rescue failing lenders that the FDIC stood poised to shut down. On May 1, JPMorgan benefited from the dispensation when it purchased virtually all the assets of First Republic from FDIC receivership, clearing the wreckage from the second largest banking failure in U.S. History, a disaster exceeded in scale only by the 2008 collapse of WaMu. Overnight, the nation’s biggest bank added significant heft, and notched what looks like a coup for its shareholders that at the same time stabilized the shaky outlook for regional banks.

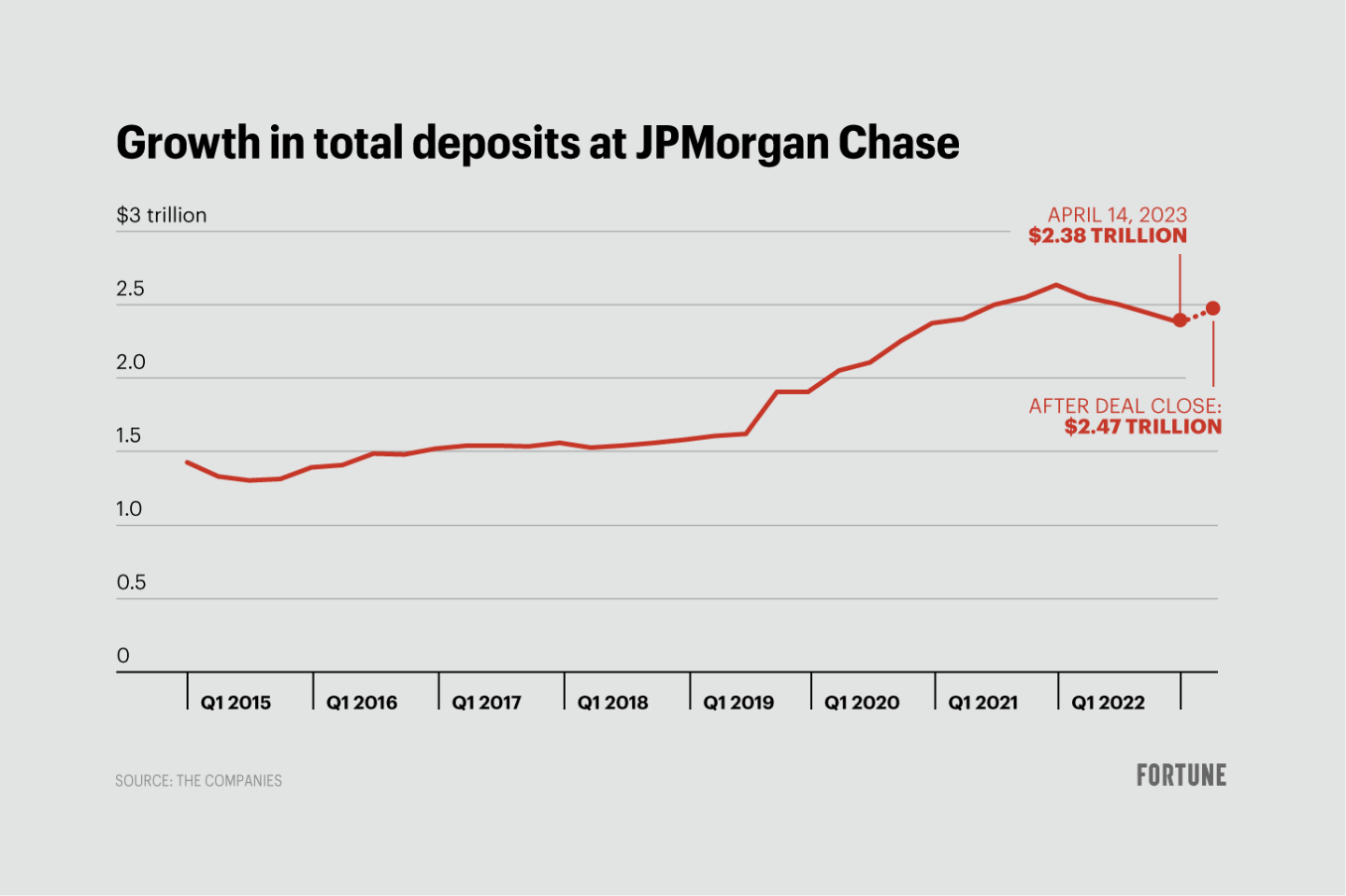

JPMorgan Chase was already leading in the deposit wars before it registered the win on First Republic

It’s interesting to trace the total deposit growth for the three biggest banks in recent years, and how the shares have shifted. In 2014, JPMorgan, B of A and Wells were locked in a virtual tie at just over 10%, and all together held 32% of the market. Since then, Wells has gone flat, while JPMorgan and B of A, by the close of 2022, had respectively grown their caches by 132% and 92%, so that combined, those two alone control 31% of all deposits, with JPMorgan out in front at 16.1%. The two leaders feasted from the lavish government aid granted during the pandemic. Those trillions in support for payrolls and cash payments to families swelled checking and savings accounts for most banks, but especially for the leading symbols of solidity, JPMorgan and B of A. Since 2019 alone, JPMorgan’s deposits have leaped 62% to $2.2 trillion.

The First Republic gambit adds $92 billion to that total in one quick grab. That additional four percent-plus may sound like a small number. But keep in mind that those dollars available for funding consumer loans and lines of credit come on top of an absolutely gigantic base. A bump of around $90 billion would have lifted Citigroup’s total by over 11%. It’s also equivalent to three-quarter of all the deposits JPMorgan tacked on from 2021 to 2022, and well above the average of $56 billion a year its stash grew from 2014 to 2019.

The deal has already boosted JPMorgan’s stock

JPMorgan landed the First Republic assets in an auction that included a number of rival bidders. Despite the competitive nature of the purchase, CEO Jamie Dimon appears to have secured highly favorable terms. Start with those $92 billion in deposits. They’re far from the “hot money” amassed from tech hotshots and super-high-net worth individuals that fled when the bad news started spreading. Many of the customers parked their millions at First Republic because it provided them with inexpensive “jumbo” home loans, a practice that Dimon declared dead on the conference calls where he and CFO Jeremy Barnun explained the transaction. JPMorgan’s acquiring the stable deposits that stayed, the paychecks that average folks bank on direct deposit and the dollars restaurants and plumbing outfits need to meet next week’s payroll. It’s essentially an addition to perhaps JPMorgan’s greatest asset, its low-cost hoard of deposits. The huge increase in rates for everything from small business to credit card loans lifts the value of that bedrock base.

The FDIC provided important protections and support, including a pledge to cover up to 80% of the losses on single family and commercial real estate loans for the next seven years. JPMorgan also gets $50 billion in FDIC financing at a fixed rate. The bank is adding $2.5 billion in equity that exceeds the expected restricting charges in 2023 and 2024 by $500 million. The expected gain in net income is $500 million a year. That would lift the bank’s earnings over the last four quarters by just 1.4%. But, as Barnum says, that estimate is conservative. Consider that First Republic earned $1.5 billion in 2022. It also boasted a big network of wealth management offices in the best markets, notably New York and California, and Dimon expressed confidence that the top of the advisors will join his shop.

Investors loved the deal, lifting JPMorgan shares by 3.1% and its market cap by $12 billion as of midday on May 1. On the calls, Dimon declared that the historic transaction “pretty much resolves” the recent threat to regional banks, and that “this part of the crisis is over.” Dimon has always emerged as a daring industry spokesman and leader in times of upheaval. In helping to solve this one, he’s also pounced on at the rarest of opportunities to grow by best of another financial institution, and grow big, safely and in a jiffy.